All Categories

Featured

Table of Contents

Misalignment can cause unneeded costs or inexible debt. A term loan supplies a xed swelling sum, paid back over a set period with foreseeable payments and a set rate. It's perfect for specic, one-time investments like devices, restorations, or acquisitions, and normally oers lower interest rates, specifically if secured. An organization line of credit is a revolving account with a limit.

How Stock Precision Cuts Store OverheadThis exibility fits money ow management, seasonal revenue gaps, payroll, or unforeseen costs. Nevertheless, this exibility usually includes higher rates of interest than a term loan. In other words, term loans nance things (e.g., purchasing an oven), while lines of credit manage cash circulation (e.g., covering a sluggish season). Many companies take advantage of utilizing both for their designated purpose.

Talking with an industrial financing professional before using can help clarify which structure makes one of the most sense for the specic usage of funds, the payment timeline that ts your service's money ow, and whether a combination of both products much better serves your business's general nancing technique. A well-prepared loan application does more than satisfy a list.

Will the Systems Scale By 2026?

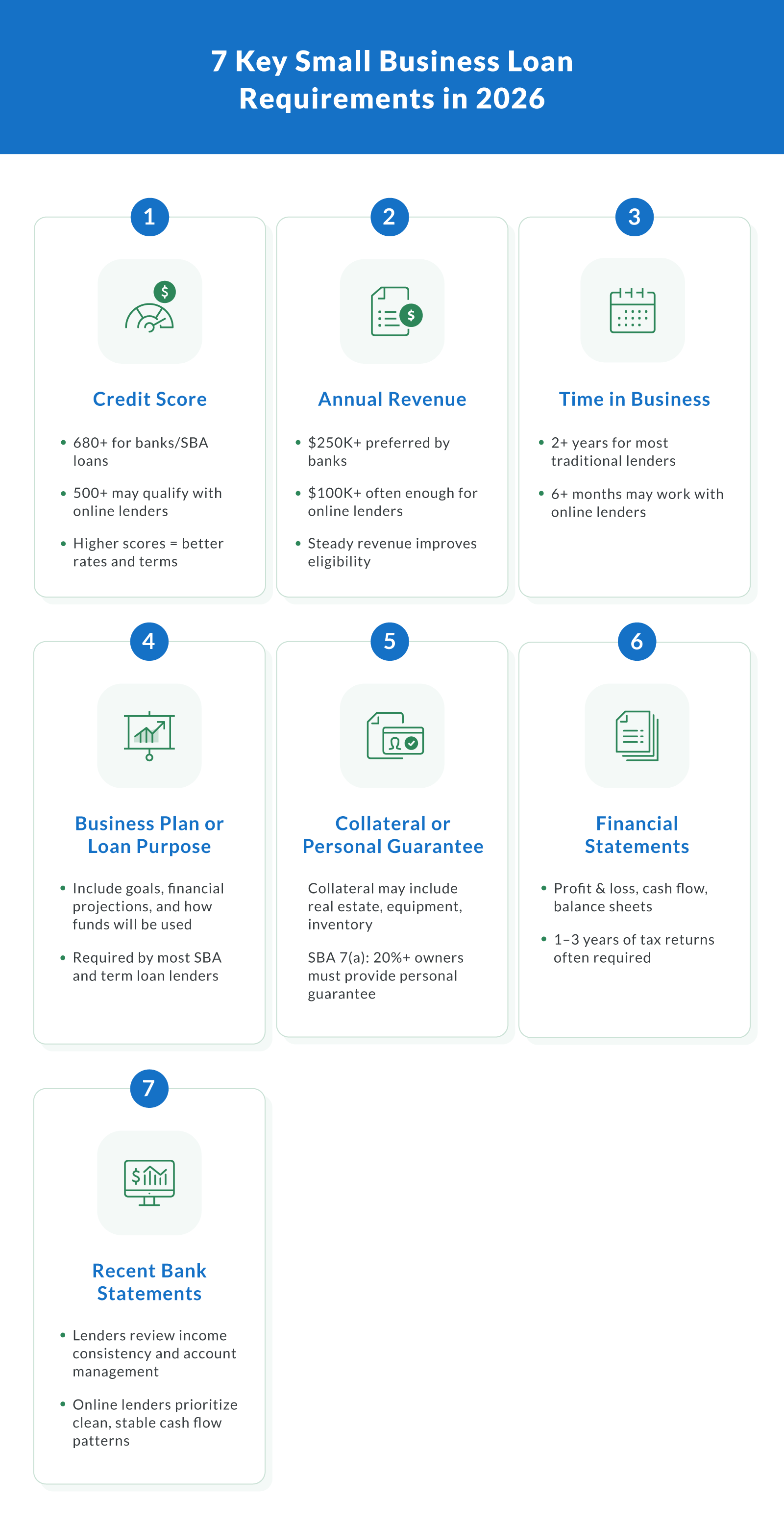

Incomplete or disorganized applications are among the most common and most avoidable factors for hold-ups and denials. Getting the paperwork right before you send puts the application in the greatest possible position from day one. The core files most lenders need include personal and organization tax returns for the past 2 to three years, current prot and loss statements, a present balance sheet, company bank statements for the past three to 6 months, and a debt schedule showing existing obligations.

The more complete and arranged the plan, the faster the underwriting procedure relocations. Lenders extremely value the Debt Service Coverage Ratio (DSCR), which measures a company's money ow against its existing and requested debt responsibilities. A minimum DSCR of 1.25, implying $1.20 in operating earnings per $1.00 of financial obligation service, is usually looked for.

Understanding your DSCR in advance permits you to resolve deficiencies or modify the loan demand. Beyond metrics, lenders require a specic, realistic loan function. Detailing how funds will be utilized, the expected return, and the repayment strategy strengthens the application. Unclear demands for "working capital" are less compelling than plainly supported growth initiatives, devices purchases, or seasonal nancing requirements.

The Complete 2026 Business Funding Approval Checklist

Many conventional loan providers require at least 2 years in organization, tidy income tax return, nancial statements, and a clear description of how earnings will be utilized, according to Small Company Trends. Gathering these files before you begin the application, rather than assembling them under deadline pressure, lowers errors and provides you a possibility to catch potential concerns, such as inconsistencies between tax returns and bank declarations, before the loan provider does.

Loan rejections are more typical than many entrepreneur anticipate entering into the process. According to nancing they sought, 36% received some or most, and 22% received none. That indicates majority of all candidates did not get completely funded. Comprehending why rejections occur and what lending institutions are really searching for offers entrepreneur a concrete path to enhancing their odds before submitting.

As covered in Section 4, customer nancials account for roughly 68% of rejection factors according to Federal Reserve lending information. Paying down existing responsibilities before applying, or using for a smaller sized amount that ts within current money ow capability, directly addresses this issue.

Practical SME Bookkeeping Tips for Protect ROI

An individual score below 650 signicantly narrows the pool of lenders happy to approve an application, and listed below 600, it ends up being really dicult outside of alternative nancing channels with less beneficial terms. Pulling your individual credit report before using, challenging any errors, and taking actions to minimize credit utilization in the months prior to sending an application can meaningfully move the number.

A lot of of credit, and many SBA lenders follow the same requirement. Companies under two years of ages are not locked out of nancing entirely, but they usually require to depend on the owner's personal credit prole more greatly, offer more powerful security, or explore SBA programs created for earlier-stage companies. Incomplete or irregular paperwork complete the most typical denial causes.

Lenders view disorganized documentation as a proxy for how business is handled. Resolving it before submission expenses nothing and removes a quickly avoidable obstacle. The most typical factors rms were rejected or underfunded were weak nancials, insucient cash ow to cover existing and new financial obligation obligations, and credit report issues.

Using AI to Boost Store Financial Sustainability

Not every company nancing need ts neatly into a term loan or credit line. For business prepared to acquire home, expand physical operations, or purchase the cars and equipment that drive income, specialized loan products oer structures much better suited to those objectives. iTHINK Financial oers both industrial realty loans and lorry and equipment nancing for Florida and Georgia companies at various stages of growth.

Terms, rates, and loan-to-value ratios vary based on residential or commercial property type, business nancials, and the customer's creditworthiness. Florida First Capital Financing Corporation (FFCFC), which serves Alabama, Florida, and Georgia, is an SBA-authorized CDC that works along with lending institutions like iTHINK Financial to structure 504 loans for qualifying businesses in the area. This type of nancing is especially appropriate for businesses in building, logistics, landscaping, health care, and other asset-intensive industries common throughout Florida and Georgia.

Leveraging Smart Staff Models to Higher Profits

The SBA 504 and 7(a) programs dier signicantly. The 7(a) is more comprehensive, covering operating capital, equipment, realty, and financial obligation renancing. The 504 is narrower, concentrating on xed possessions like realty and significant devices, however oering higher loan amounts and lower down payments for those uses. For Florida or Georgia organizations getting home or significant devices, the 504 typically provides much better terms than a conventional CRE or 7(a) loan.

SBA loan timelines can differ from a couple of weeks to a couple of months based on the lending institution, loan amount, and general application completeness. Among the most eective ways to avoid delays is to send a fully complete application upfront, consisting of tax returns, nancial statements, a service strategy, and individual nancial declarations.

{kind=link}

Latest Posts

Efficient Staff Scheduling Tactics for Peak Productivity

How Digital Inventory Management Systems Cut Waste

Traditional Vs Automated Inventory Control