All Categories

Featured

Table of Contents

Not every service nancing require ts neatly into a term loan or credit line. For business prepared to obtain property, broaden physical operations, or buy the cars and devices that drive earnings, specialized loan products oer structures better fit to those objectives. iTHINK Financial oers both business property loans and vehicle and equipment nancing for Florida and Georgia services at numerous phases of growth.

Terms, rates, and loan-to-value ratios vary based on home type, company nancials, and the debtor's creditworthiness. Florida First Capital Financing Corporation (FFCFC), which serves Alabama, Florida, and Georgia, is an SBA-authorized CDC that works alongside lenders like iTHINK Financial to structure 504 loans for qualifying services in the region. This type of nancing is particularly appropriate for companies in construction, logistics, landscaping, health care, and other asset-intensive industries typical throughout Florida and Georgia.

Combining Automation and Boost SME Fiscal Sustainability

The SBA 504 and 7(a) programs dier signicantly. The 7(a) is wider, covering working capital, equipment, realty, and debt renancing. The 504 is narrower, focusing on xed assets like property and significant devices, however oering greater loan amounts and lower deposits for those uses. For Florida or Georgia businesses acquiring property or major devices, the 504 typically provides better terms than a traditional CRE or 7(a) loan.

SBA loan timelines can differ from a few weeks to a few months based on the lending institution, loan amount, and general application completeness. One of the most eective ways to prevent hold-ups is to submit a fully total application upfront, consisting of tax returns, nancial declarations, an organization strategy, and individual nancial statements.

A standard term loan lacks this government backing, leading to more stringent underwriting and shorter payment terms, however possibly a much faster approval for strong borrowers. The best choice depends on the borrower's nancial scenario, fund usage, and desired repayment exibility.

Using Automation to Improve SME Financial Sustainability

Prospective debtors in Florida and Georgia can examine eligibility and open membership through ithink.org before or along with beginning the loan application procedure. For organizations specically checking out SBA nancing, iTHINK Financial's SBA loan page details available programs and how to start with our lending team.

SBA loans use practical financial alternatives for almost any business purpose. As a U.S. Small Service Administration (SBA) Preferred Lending institution, we can show you how to put these SBA programs to work for your service.

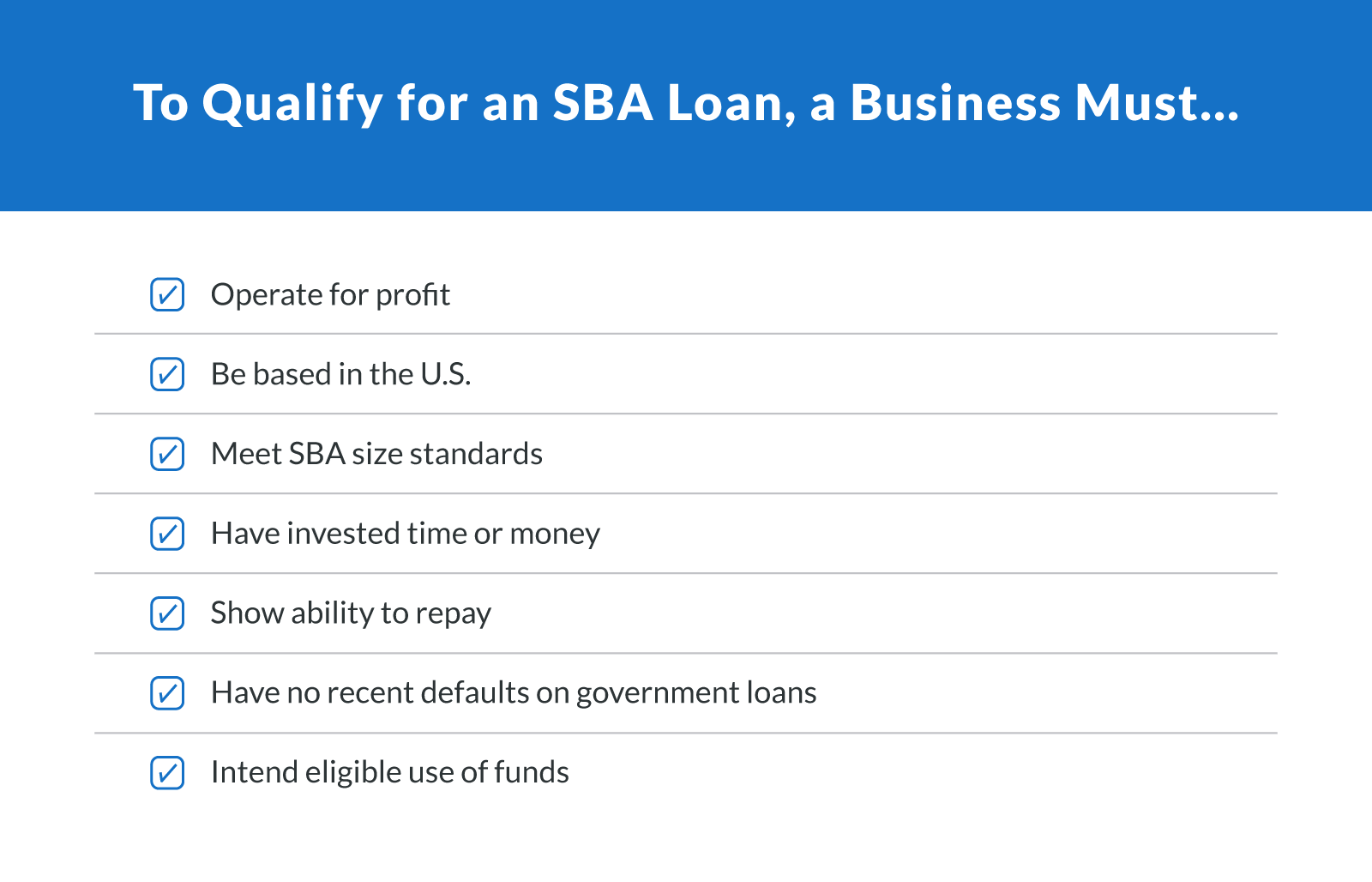

Your organization is legally organized as a sole proprietorship, corporation, partnership or LLC.

Navigating Key Business Funding Criteria in 2026

U.S. Small Company Administration (SBA) loans are popular because they often use competitive rates and longer repayment terms. The SBA ensures a portion of these loans, which can reduce threat for loan providers and make funding more accessible to small companies. Each SBA loan program has its own rules, and lending institutions may apply additional underwriting requirements.

Program requirements, rates, and eligibility are present since and may change. Constantly validate the newest information with an SBA-approved lending institution. SBA's present guidance likewise shows a March 1, 2026 update to citizenship and residency guidelines, and a March 1, 2026 change to how SBSS is dealt with for 7(a) Small Loans.

A standard term loan lacks this government backing, leading to more stringent underwriting and shorter payment terms, however potentially a faster approval for strong debtors. The finest choice depends on the debtor's nancial situation, fund use, and preferred repayment exibility.

Prospective customers in Florida and Georgia can inspect eligibility and open membership through ithink.org before or along with beginning the loan application procedure. For companies specically exploring SBA nancing, iTHINK Financial's SBA loan page outlines readily available programs and how to get going with our loaning team.

SBA loans provide practical monetary options for nearly any organization purpose. These programs use long terms, low deposits and reduced security requirements. As a U.S. Small Company Administration (SBA) Preferred Loan provider, we can show you how to put these SBA programs to work for your service. Certifications: You own and run a for-profit organization.

Traditional Versus Digital Inventory Tracking

Your company is lawfully arranged as a sole proprietorship, corporation, partnership or LLC.

U.S. Small Organization Administration (SBA) loans are popular since they frequently offer competitive rates and longer repayment terms. The SBA ensures a portion of these loans, which can minimize risk for loan providers and make funding more accessible to small companies. Each SBA loan program has its own rules, and loan providers might apply additional underwriting requirements.

Program requirements, rates, and eligibility are current since and might change. Constantly confirm the most recent details with an SBA-approved lending institution. SBA's existing assistance also reflects a March 1, 2026 upgrade to citizenship and residency rules, and a March 1, 2026 change to how SBSS is dealt with for 7(a) Small Loans.

{kind=link}

Latest Posts

Efficient Staff Scheduling Tactics for Peak Productivity

How Digital Inventory Management Systems Cut Waste

Traditional Vs Automated Inventory Control